When Tony realized his 15-year-old furnace was wheezing through another Ohio winter, his first thought wasn’t about SEER2 ratings or BTUs. It was: “How am I going to afford this?”

Replacing an HVAC system is a big financial decision. Most modern systems can run anywhere from $5,000 to $15,000+ depending on size, efficiency, and installation complexity. That’s not the kind of expense most families have sitting in a savings account.

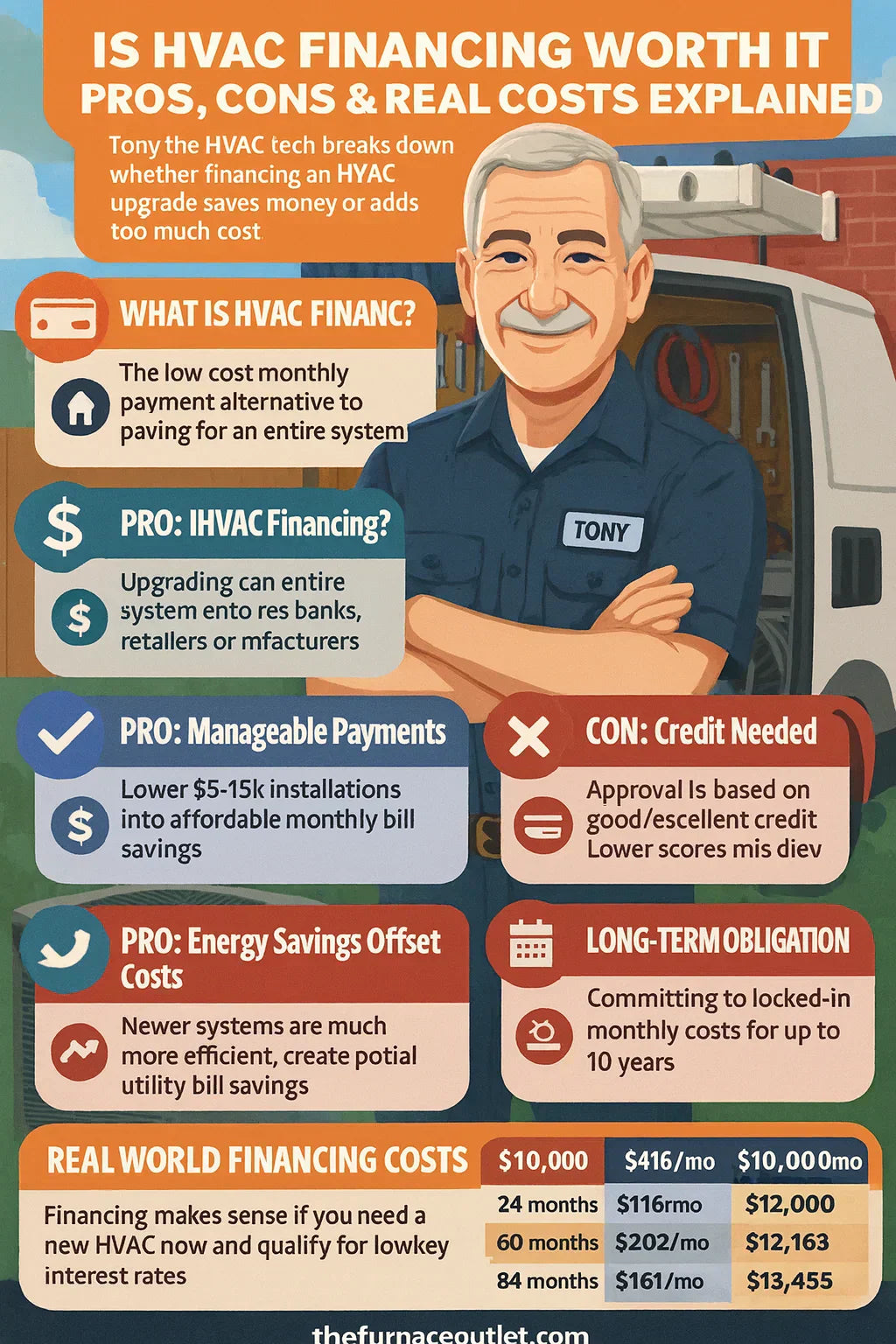

This is where HVAC financing comes into play. But is it truly worth it—or does it cost more in the long run? Let’s break it down for Tony (and homeowners like him), covering pros, cons, and real-world costs.

📌 What Is HVAC Financing?

HVAC financing is essentially a loan or payment plan that allows homeowners to pay for a new heating and cooling system in monthly installments instead of one large upfront payment.

Financing can come in several forms:

-

Manufacturer financing (through companies like Goodman, Carrier, or Trane)

-

Retailer or contractor financing (through partners like Synchrony Bank or Wells Fargo Home Projects)

-

Personal loans or credit cards (less favorable due to high interest)

-

Utility company programs (sometimes available for energy-efficient upgrades)

Instead of writing a $10,000 check, Tony could break that into payments of $150–$250 per month, depending on his credit, term length, and interest rate.

✅ The Pros of HVAC Financing

1. 🏡 Immediate Comfort Without the Wait

For Tony, waiting another winter wasn’t an option. Financing allows families to replace or upgrade HVAC systems immediately, even if they don’t have the cash.

2. 💵 Manageable Monthly Payments

A $10,000 system can be intimidating upfront, but when split into affordable monthly payments, it becomes much more manageable—like a car payment.

👉 Example: On a 5-year loan at 8% APR, $10,000 becomes roughly $202 per month.

3. ⚡ Energy Savings Offset Costs

Newer systems are far more efficient. According to the U.S. Department of Energy, upgrading to a high-efficiency AC can cut cooling costs by 20–40%. That means some of Tony’s monthly payment might be offset by lower utility bills.

4. 🎁 Access to Better Equipment

Financing lets homeowners choose higher-efficiency models they might not otherwise afford. Over 10–15 years, that efficiency often saves more than the added financing costs.

5. 🛠️ Full Installation & Warranty Included

Most financing plans cover equipment + installation, and Tony can often bundle extended warranties or maintenance plans into the loan.

6. 🧾 Potential Tax Credits & Rebates

Energy-efficient upgrades may qualify for incentives like the Inflation Reduction Act tax credits or utility rebates. Financing spreads out the cost while still letting Tony claim the benefits.

⚠️ The Cons of HVAC Financing

1. 💸 Interest Costs Add Up

The biggest drawback: you pay more over time. Interest rates can range from 0% promotional offers to 20%+ (if using credit cards).

👉 Example: At 10% APR over 5 years, that same $10,000 system ends up costing $12,748.

2. 📉 Approval Depends on Credit

Tony’s credit score matters. Poor credit can mean higher rates, shorter terms, or even denial.

3. 🕒 Long-Term Obligation

Financing stretches payments out over 3–10 years. That means committing to monthly bills even if other financial needs come up.

4. 🧾 Fine Print on Promotions

Zero-interest deals sound amazing, but many have deferred interest clauses. If Tony misses a payment or fails to pay off the balance in time, he could be charged retroactive interest.

5. 💳 Other Debt Load

Adding an HVAC loan to existing debts (car, student loans, credit cards) may strain household budgets.

📊 Real Costs: How Financing Changes the Price

Let’s look at real-world scenarios for Tony.

Example: $10,000 HVAC System

| Term | APR | Monthly Payment | Total Paid |

|---|---|---|---|

| 24 months | 0% | $416.67 | $10,000 |

| 60 months | 8% | $202.76 | $12,165 |

| 84 months | 9.5% | $160.20 | $13,454 |

👉 The longer the term, the smaller the monthly payment—but the higher the total cost.

🏦 Types of HVAC Financing Options

1. 🏢 Contractor/Dealer Financing

Most contractors partner with lenders like Synchrony or Wells Fargo. This is the most common route, and often includes promotional 0% APR offers for qualified buyers.

2. 🏭 Manufacturer Financing

Brands like Lennox, Trane, Goodman often run financing promotions tied to rebates or seasonal deals.

3. 💳 Credit Cards

If Tony puts $10,000 on a card at 20% APR, he could end up paying nearly double the system cost if not paid quickly. Risky unless using a 0% intro APR card.

4. 🏦 Personal or Home Equity Loans

Banks and credit unions may offer personal loans (7–15% APR) or HELOCs (lower APR but risk to your home if you default).

5. 🔌 Utility Company Programs

Some local utilities offer on-bill financing—Tony pays for the system through his monthly energy bill. Example: PG&E’s Energy Efficiency Financing.

🧾 Real-World Example: Tony’s Case

Tony lives in a 2,400 sq. ft. Ohio home. His contractor quotes him $11,500 for a Goodman 3-ton heat pump system with air handler.

-

Option 1: Pay cash upfront → $11,500

-

Option 2: Finance with Wells Fargo at 0% APR for 24 months → $479/month, total $11,500

-

Option 3: Finance with Synchrony at 8.9% APR over 72 months → $202/month, total $14,544

👉 For Tony, if he can swing the 24-month 0% promo, financing makes perfect sense. But if he stretches to 72 months, he pays $3,000+ more.

🧠 Tips Before You Finance

-

Check Credit First – Use AnnualCreditReport.com to review your score before applying.

-

Read the Fine Print – Look for deferred interest, fees, or penalties.

-

Compare Lenders – Don’t just take the first offer; shop between contractors, banks, and credit unions.

-

Use Promotions Wisely – A 0% APR deal can save thousands—but only if you can pay it off in time.

-

Factor Energy Savings – Higher-efficiency systems may actually offset financing costs with lower utility bills.

🔮 Is It Worth It? The Bottom Line

For Tony—and most homeowners—HVAC financing is worth it when:

-

A system replacement is urgent (broken furnace/AC).

-

You qualify for 0% or low-interest promotional rates.

-

You choose a system that saves enough on utilities to offset interest.

-

You can comfortably fit the monthly payment into your budget.

But financing can be risky if:

-

You accept high-interest long-term loans.

-

You fail to read fine print on deferred interest deals.

-

You’re already overextended on debt.

In short: HVAC financing is a powerful tool—but only if used wisely.

In the next topic we will know more about: HVAC Financing vs. Credit Cards vs. Personal Loans: Which One Saves You More?