When Tony saw an HVAC dealer’s advertisement claiming “New system for just $150/month!” he raised an eyebrow. He had an important question:

“Does that payment include installation, warranties, and maintenance—or is it just the box sitting on my driveway?”

This is one of the most common (and overlooked) questions homeowners ask when exploring HVAC financing. The truth is, what’s covered in financing depends on the lender, the contractor, and the specific plan.

In this guide, we’ll walk through what’s included in typical HVAC financing, what’s optional, and what’s not covered at all—so homeowners like Tony know exactly what they’re paying for.

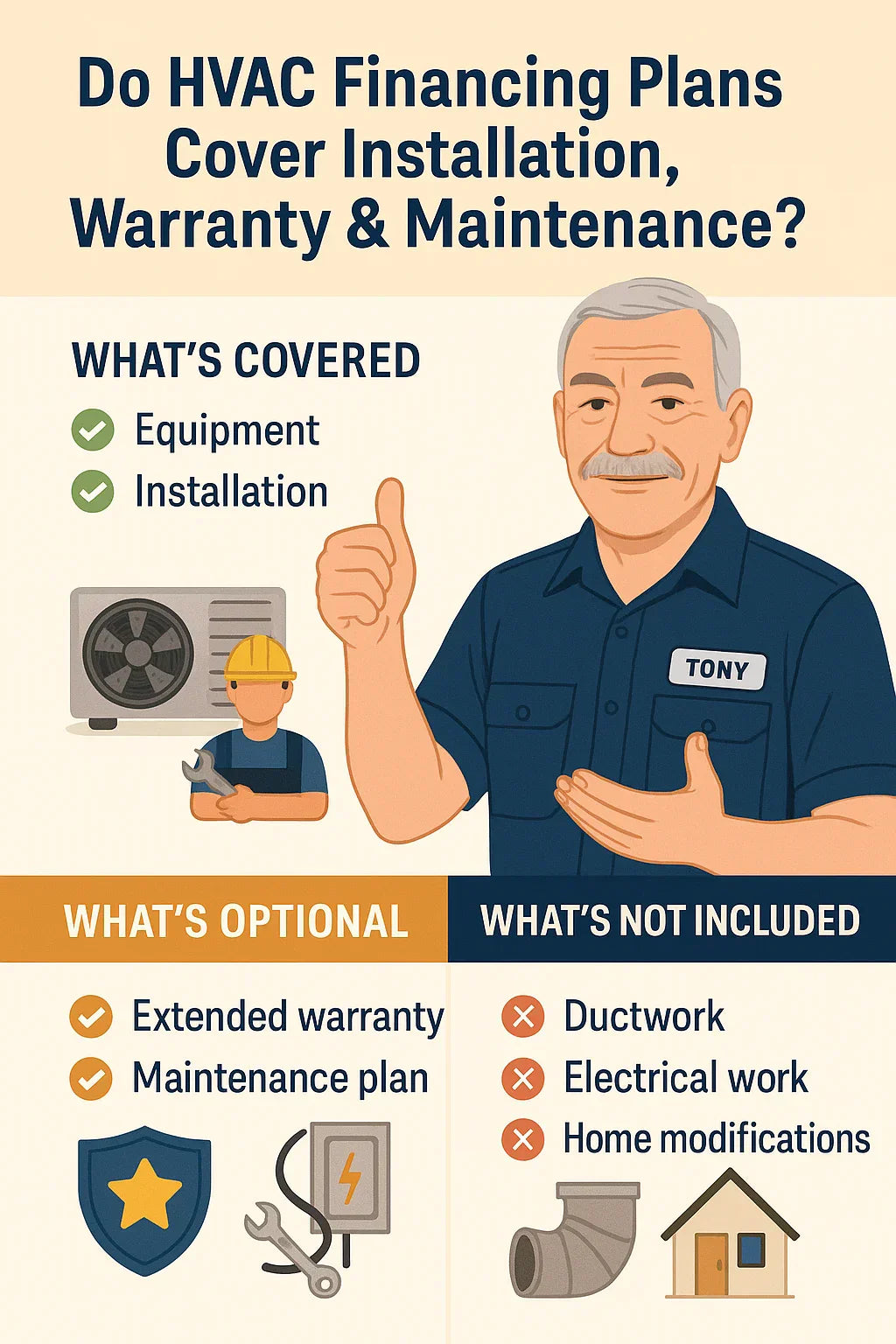

📦 What HVAC Financing Usually Covers

In most cases, HVAC financing is structured to cover the full system replacement package—not just the equipment itself. That means:

-

✅ Equipment (furnace, AC, heat pump, air handler)

-

✅ Installation labor (setup, removal of old unit, basic connections)

-

✅ Permits and inspection fees (required by many cities)

👉 Example: Tony finances a $10,000 HVAC replacement package. About $6,000 is equipment and $4,000 is labor, permits, and installation costs—all rolled into one loan.

This bundled approach is convenient because most homeowners don’t want to manage separate payments for equipment and labor.

🛠️ Installation Costs and Financing

Installation isn’t just a side cost—it’s often 30–50% of the total project price.

-

Central AC installation: $3,000–$5,000 labor

-

Furnace installation: $2,000–$4,000 labor

-

Heat pump installation: $3,500–$6,000 labor

(Source: HomeAdvisor, Forbes Home)

The good news? HVAC financing almost always includes installation. Dealers want to keep the process simple, and lenders prefer one bundled loan.

👉 For Tony, that means his $150/month financing offer is almost certainly for a complete system + labor, not just the hardware.

🧾 Warranties in HVAC Financing

Every HVAC purchase comes with a manufacturer warranty, usually covering parts for 5–10 years. This is included at no extra charge.

But what about extended warranties and labor warranties?

-

Extended parts & labor warranties can often be added for $500–$1,500.

-

Some contractors bundle these into financing if the homeowner asks.

-

Example: Tony adds a 10-year extended labor warranty for $800. His 60-month financing goes from $202/month → $215/month.

👉 Pro tip: Extended warranties are optional, but financing them makes sense if you want predictable coverage.

🧰 Maintenance Plans in Financing

Routine maintenance keeps HVAC systems efficient and under warranty—but does financing cover it?

-

Basic manufacturer warranty does not cover tune-ups.

-

Many contractors sell annual maintenance plans ($200–$400/year).

-

Some allow homeowners to roll these into financing.

👉 Example: Tony adds a 3-year maintenance plan ($900 total). Instead of paying upfront, he finances it—adding about $15/month to his bill.

📊 Example Breakdown of a Financed HVAC Package

Let’s break down what Tony’s $12,000 financed HVAC package might look like:

| Item | Cost | Included in Financing? |

|---|---|---|

| Equipment (AC + Furnace) | $7,000 | ✅ Yes |

| Installation Labor | $4,000 | ✅ Yes |

| Permits/Inspection Fees | $300 | ✅ Usually |

| Extended Warranty (10 yrs) | $800 | ✅ Optional add-on |

| Maintenance Plan (3 years) | $900 | ✅ Optional add-on |

👉 Tony’s financing total: $12,000–$13,500 depending on add-ons.

⚠️ What’s Not Usually Covered

This is where homeowners get surprised. Not all project costs are bundled into HVAC financing. Common exclusions include:

-

❌ Ductwork replacement or major repairs ($1,000–$5,000).

-

❌ Electrical panel upgrades (needed for high-power systems, $1,000–$3,000).

-

❌ Home modifications (structural work, new vents, carpentry).

-

❌ Cosmetic extras (smart home integration, zoning upgrades, humidifiers).

👉 If Tony’s old ducts were leaky, he might need to finance a separate loan or pay cash for that portion.

🧠 Tony’s Takeaways

From Tony’s perspective:

-

Installation? Covered. Financing almost always includes labor.

-

Warranties? Sometimes. Standard warranty = included, extended = optional add-on.

-

Maintenance? Optional. Can be rolled in if the contractor offers it.

-

Hidden costs? Not covered. Ductwork, electrical, or structural changes may require separate payment.

🧾 Real Financing Scenarios

Here’s how Tony’s payment might change based on what’s included:

| Scenario | System Cost | APR | Term | Monthly Payment | Total Paid |

|---|---|---|---|---|---|

| Basic System + Install | $10,000 | 8% | 60 mo | $202 | $12,165 |

| + Extended Warranty | $10,800 | 8% | 60 mo | $218 | $12,999 |

| + Warranty + Maintenance Plan | $11,700 | 8% | 60 mo | $236 | $14,163 |

👉 Tony’s $202/month payment grows to $236/month once warranty and maintenance are added—but it gives him full peace of mind.

🔍 How to Make Sure You Know What’s Included

-

Ask for a detailed breakdown – Equipment, labor, warranties, add-ons.

-

Request a separate line for maintenance plans – so you can choose.

-

Check if ductwork is covered – many homeowners get surprised by this extra cost.

-

Compare multiple quotes – financing terms vary between contractors.

⚡ Energy Savings Offset Costs

Tony also realized that energy savings can help offset financed add-ons.

-

New high-efficiency systems cut bills by 20–40% (DOE).

-

If Tony saves $80/month on utilities, adding a $15/month maintenance plan feels like a bargain.

🔮 Conclusion: What HVAC Financing Really Covers

For Tony—and most homeowners—the answer is:

-

Installation: ✅ Almost always included

-

Warranty: ✅ Standard included, extended optional

-

Maintenance: ✅ Optional, sometimes offered as financing add-on

-

Extras (ductwork, electrical, home mods): ❌ Usually not included

Bottom line: HVAC financing can cover more than just the system itself, but you need to ask what’s bundled. Always get a line-item breakdown before signing so you’re not caught off guard.

In the next topic we will know more about: How Long Should You Finance an HVAC System? 24, 36, or 60 Months?