When Tony’s 17-year-old furnace stopped working during the first cold snap of winter, he panicked. A new HVAC system would cost him $8,000–$12,000, and he didn’t have that kind of cash on hand. To make things worse, his credit score had slipped below 600 after a rough few years.

His first thought: “Will any company even approve me for financing with bad credit?”

If you’ve been in Tony’s shoes, you’re not alone. Many homeowners with fair or poor credit (below 650) worry that HVAC financing isn’t an option. The truth? You can qualify, but you’ll need to know where to look, how to compare offers, and what alternatives exist.

This guide breaks down what lenders look for, financing options with bad credit, alternatives, and smart tips for getting the system you need without breaking the bank.

🏠 Why Credit Score Matters for HVAC Financing

When you apply for HVAC financing, lenders want to know how risky you are as a borrower. Your credit score is their quick snapshot of that risk.

-

Good credit (670–739): Best approval odds, lower APRs (6–10%), and promotional offers (like 0% for 24 months).

-

Fair credit (580–669): Approval possible, but interest rates climb (10–20%+).

-

Poor credit (below 580): Harder to qualify, higher APRs (20–30%), shorter repayment terms.

👉 Tony, with a score under 600, might still qualify—but likely at a higher interest rate or with extra conditions.

📌 What Lenders Look At Besides Credit Score

Even if your score isn’t great, lenders also consider:

-

Income level – steady income improves approval chances.

-

Employment status – proof of employment helps.

-

Debt-to-income ratio – if your debts eat up too much of your income, approval is harder.

-

Co-signers – having a co-signer with good credit can unlock better terms.

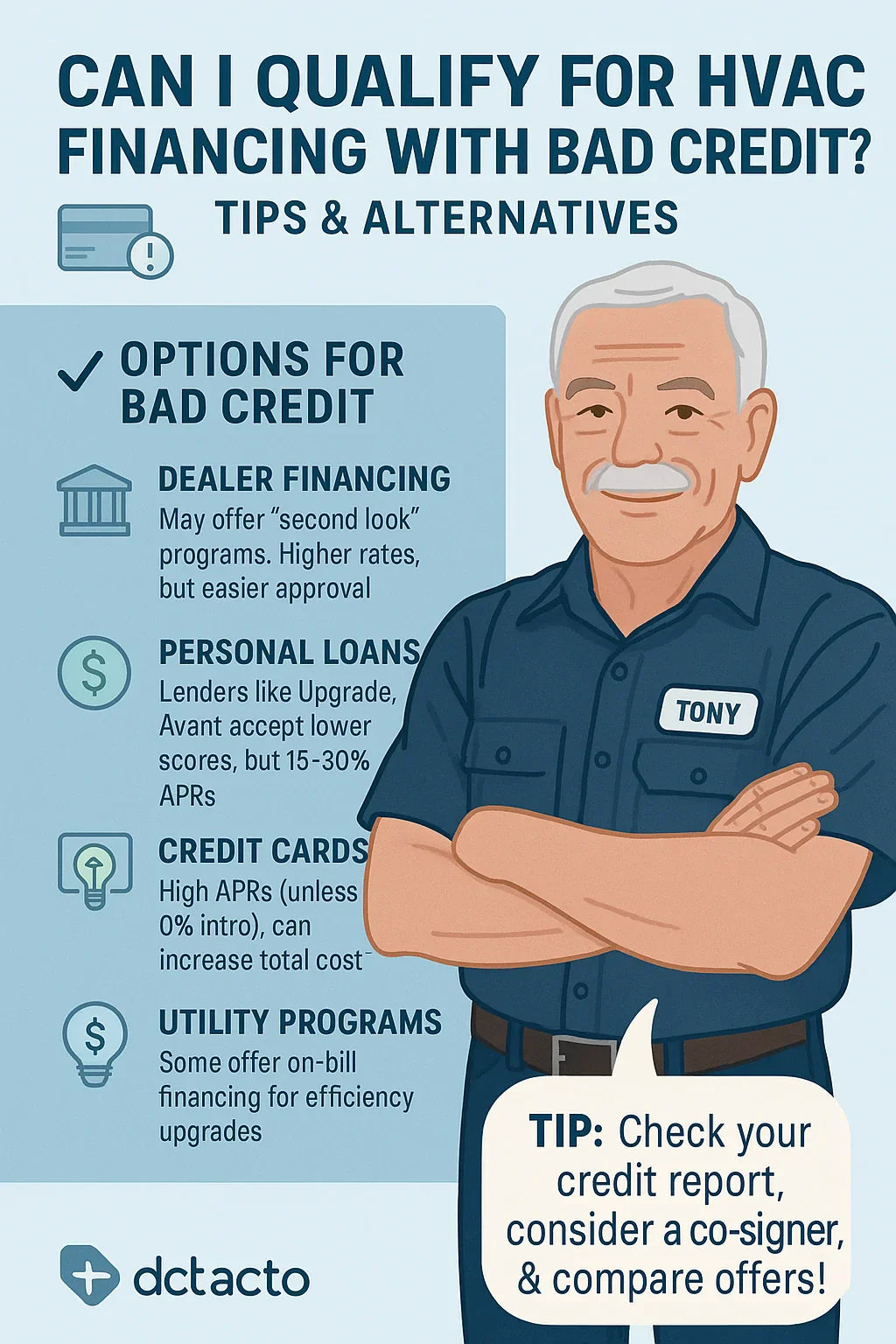

✅ Financing Options for Bad Credit

1. 🏢 Dealer/Contractor Financing

Most HVAC contractors partner with financing companies like Synchrony Bank or Wells Fargo Home Projects.

-

Pros: Easy to apply through your installer, sometimes “second look” programs for lower credit.

-

Cons: Higher APRs for poor credit, possible deferred interest traps.

👉 Example: Tony applies through his dealer and is approved for 60 months at 17.9% APR. His $10,000 system becomes $255/month, $15,300 total.

2. 🏦 Personal Loans for Bad Credit

Some lenders specialize in “fair” or “poor” credit borrowers. Examples: Avant, Upgrade.

-

APR Range: 15–30% depending on score.

-

Loan Terms: 24–60 months typical.

-

Pros: Predictable payments, cash in hand for any contractor.

-

Cons: Higher rates and potential origination fees.

👉 Example: $10,000 at 22% APR over 60 months → $276/month, $16,560 total.

3. 💳 Credit Cards

Tony thought about swiping his existing card. But here’s the reality:

-

Pros: Fast approval if you have available credit, possible rewards.

-

Cons: Regular APRs are brutal—18–25%. Only worth it if you qualify for a 0% intro APR card and pay it off within the promo period.

👉 Example: $10,000 at 20% APR over 60 months → $265/month, $15,900 total.

4. 🔌 Utility or Government Programs

Some utilities and state energy offices offer on-bill financing for HVAC upgrades.

-

Payments are added to your utility bill.

-

Often low or no interest.

-

May not require a high credit score.

👉 Example: Energy.gov lists state-by-state programs like PACE loans or local utility financing.

🧾 Alternatives If You Don’t Qualify

If financing isn’t an option, Tony still has choices:

-

Rent-to-Own HVAC Programs

-

No credit check required.

-

Pay monthly, own after term.

-

Downside: higher long-term cost.

-

-

Manufacturer Rebates & Federal Tax Credits

-

Rebates from brands like Trane or Goodman can cut $500–$1,000+.

-

Energy Star federal tax credits cover up to 30% of costs (max $2,000) for qualifying systems.

-

-

Home Equity Loans or HELOCs

-

Lower APRs (6–9%), longer repayment terms.

-

Risk: your home is collateral.

-

-

“Buy Now, Pay Later” Apps

📊 Example Payment Scenarios (Bad Credit)

| System Cost | APR | Term | Monthly Payment | Total Paid |

|---|---|---|---|---|

| $10,000 – Dealer “Second Look” | 17.9% | 60 mo | $255 | $15,300 |

| $10,000 – Personal Loan | 22% | 60 mo | $276 | $16,560 |

| $10,000 – Credit Card | 20% | 60 mo | $265 | $15,900 |

| $10,000 – Utility Financing | 5% | 60 mo | $189 | $11,340 |

👉 With bad credit, the difference in total cost can be $5,000–$6,000, depending on the program chosen.

🧠 Tips to Improve Your Chances

Even with bad credit, Tony can improve his odds of approval:

-

Check Your Credit First – Use AnnualCreditReport.com to review.

-

Pay Down Small Debts – Lowering balances quickly improves score.

-

Avoid Payday Loans – High-risk and predatory.

-

Look for Co-Signers – Partnering with a family member with good credit can unlock better terms.

-

Ask About “Second Look” Programs – Some financing companies specialize in lower-score borrowers.

🧮 Energy Savings Can Still Help

Tony realized that while his interest costs would be higher, his monthly energy bills would be lower with a new high-efficiency HVAC.

-

His old system: $280/month peak season.

-

New system: $180–200/month.

-

Savings of $80–100/month.

👉 That savings offsets part of his financing payment—even with higher APR.

🔮 Conclusion: Tony’s Bad Credit Options

So, can Tony qualify for HVAC financing with bad credit? Yes—but the terms won’t be as attractive.

-

If approved through dealer/utility programs: He gets his system installed quickly, but pays more in interest.

-

If denied: He can explore rent-to-own, rebates/tax credits, or a co-signer.

-

Best long-term move: Improve credit, then refinance to a lower-interest loan.

Bottom line: Bad credit doesn’t mean no options—it just means you need to be strategic, cautious, and informed.

In the next topic we will know more about: Do HVAC Financing Plans Cover Installation, Warranty & Maintenance?